Lucinda

|

|

In startups, speed is critical. Why?

You’ll often hear that the drive for speed is to beat the competition. Although this is certainly true sometimes, I think that the consistent, foundational reason is closer to home: burn. When you’re running a venture-backed startup you’re burning cash, and the cost of anything is the time it takes. So, for example, if you’re testing a marketing tactic that costs $10,000, you’re likely to think that the cost is $10,000. It is not. Say you’re burning $100,000 a month and it takes you a week to decide and a week to run the test the cost is $60,000! That’s $10,000 for the spend plus 2 weeks of burn. You control the cost by shortening the time: decide over the weekend and run the test in a week and its cost is $35,000. So how do you move fast? Almost always, you’re doing something that has never been done. That means that results are unpredictable–there’s no playbook. You have no idea if the way you’re approaching your problem will work. A natural reaction to the situation is to plan, to think hard about what your very best guess is, to try to beat the odds. But that’s exactly the wrong thing to do. In 1996 I was running product at Infonautics, an early Internet company, working for successful serial entrepreneur and famous venture capitalist Josh Kopelman. It was very early days on the Internet and the extremely fast pace of unpredictable change made decisions especially hard. I walked into his office to brainstorm the right approach to a major partnership and he said: Imagine we’re in an alley with only one way out and it’s pitch dark. Most people inch forward slowly, arms outstretched, to ensure that they don’t run into a wall, then feel around the edges to find the way out. The right thing to do is put your head down and run as fast as you can in any direction. When you hit the wall, you have learned one way that is not out. Pick yourself up and run just as fast in the opposite direction. You’ll find the opening before the careful person has found one wall. This was decades before Lean Startup codified the approach - but the idea was the same: act and learn. Another way to think about this is in purely in terms of time. In venture-backed startups we raise a round of financing to reach certain objectives that qualify us for the next round, at an increased valuation. So, for example, you might have achieved product market fit (people want what you have) but not yet go to market fit (they find you and buy.) Say you raise $3m, which should last you about 18 months burning about $150,000 a month. If every test takes a month, you can try 18 times. If every test takes you two months, you can try 9 times, and so on. I have seen startups blow an entire round on a single theory. The right answer is rarely obvious, so give yourself as many at-bats as possible. It’s uncomfortable to knowingly run headlong into a wall, especially for people who have learned that careful planful behavior leads to success. It’s counter-intuitive. It’s also fun.

0 Comments

We’re Building a New Company, AboveBoard, to Change Executive Search and Thereby the World10/19/2020 I have founded a company called AboveBoard which launched today. This will come as a surprise to many who know me: I am supposed to be retired. I certainly didn’t expect to launch a brand new venture at this stage. So why this company, and why now? I am lucky to have had a great career as a serial entrepreneur that has taken me a long way from where I began: after starting out in tech as a secretary 30+ years ago, I went on to found three companies and lead two others before stepping down in 2018 to care for a daughter who was losing a 5-year battle with Lyme disease. I just couldn’t be a good Mom and a good CEO—and Mom wins. So I transitioned into the classic executive “retirement” of serving on boards and advising startup CEOs. It was enjoyable work, and as my daughter started to recover I expected to continue on that track. Throwing myself into a new venture is a (happy) surprise. Why do it again? I feel called. AboveBoard represents both an enormous market opportunity and an expression of my deepest-held personal values. I founded AboveBoard because we have a clear path to creating a fundamental shift in the dynamics of executive hiring, one that is way overdue and will have far-reaching social impact. AboveBoard addresses a gaping chasm in a huge market. Today, when a company decides to hire an executive or board member, there are only have two options: do it themselves or hire a retained executive search firm. Either way, it’s a closed process with no transparency: those roles aren’t posted on LinkedIn or made public in any way. Retained search (or headhunting) is a great model for some situations, but there’s no reason for it to be the only available option. There is tremendous opportunity in offering a new approach with a new value proposition. And, it turns out, this lack of hiring options is directly tied to an immediate and pressing need: diversity. In the past few years demand from companies to interview more diverse slates of candidates has been growing, and it’s reaching a new peak. It turns out that the current lack of diversity and the lack of alternatives in search are actually the same problem! How does that work? Companies that recruit directly reach out to their networks, and headhunters reach out to their networks, and both of those networks are (unintentionally) exclusionary. People tend to know people who look like them, and since neither companies nor search firms are diverse, their networks aren’t either. I had plenty of personal experience with this in my years leading and hiring at my companies—even when businesses are strongly motivated to hire for diversity, it’s hard to translate that intention into action. If we want a different result, we’ll need a different approach. I came to understand all of this while I was Chairman of Thrive TRM. Thrive is a SaaS platform used by executive recruiters inside search, private equity, and venture capital firms as well as large corporations. It was started by True Search, a crazy successful search firm focused on the growth ecosystem that I had known since their founding as a client and candidate. I had enormous respect for True: the firm is growing by bringing rare innovation to an otherwise stale industry, and making smart investments in initiatives like Thrive. The firm’s co-CEOs Brad Stadler and Joe Riggione are tremendously successful, big thinkers who know their industry inside-out and think about it in a uniquely innovative way while staying humble and down to earth. As Chairman of Thrive, I spent a day a week at True’s headquarters, and I learned search from them, from the inside. Working with Brad and Joe, as well as Reed Flesher and the entire team at Thrive, I came to understand the scale of the opportunity. And with that realization, the stars aligned: my daughter was recovering, I loved working with the True team, we had identified an enormous market opportunity and a compelling offering, and it tackled an issue I felt strongly about. We enlisted two outstanding engineers from the Thrive team, John Parsons and Marni Duffy, to build the product, and I started selling. Then George Floyd was murdered. Christian Cooper was profiled for birding in Central Park. And countless similar stories rose into the general public’s awareness all at once. Due to COVID we were all stuck in our homes with no distractions or excuses, and for the first time, white people couldn’t look away. Many, I believe, began to genuinely recognize systemic racism that they had long looked past. As the backdrop for this new venture grew into a broader national reckoning, I could feel the threads of my personal, political, and professional lives coming into alignment. I grew up on the boundary between Bed-Stuy and Clinton Hill in Brooklyn, New York, in the 60s and 70s. My block was white, Korean, and Indian, but sat within an otherwise all-Black neighborhood. I learned early on that real diversity is complicated, never as simple as a stock photo of a Black and a white toddler holding hands. As a teen I was the only white girl on my city basketball team, and at 6’1” and blonde I really stood out. My teammates called me “light bulb” and looked out for me. We had mutual trust and a strong bond. But I also witnessed disturbing incidents that revealed the subtle, and not-so-subtle, ways that my Black friends suffered fundamental injustice. I remember one Fourth of July, when the uncle of an Italian American family a couple houses over pulled into our alley in his patrol car and opened up a trunk full of illegal fireworks that he’d collected for his nieces and nephews. He laughed about having taken them from kids in the neighborhood. As a pre-teen I had a strong sense that something was very wrong with that—I didn’t understand it fully, but like all children, I could sense the injustice, I knew that the rules weren’t being equally applied. A decade later I witnessed the logical conclusion of those unspoken rules. I was coming home late on the subway and switching trains at West 4th Street. The subway in those days was gritty and crime-ridden, and we used to carry a dime and a token in our socks to call and ride home in case we were mugged. I never was. But that night, when I passed through the empty level at the north end of the station, I witnessed a terrible thing. A cop with a billy club in his hand stood behind a Black man on his knees, handcuffed, facing the white tile wall. I heard the thud as he struck him. I remember vividly the metallic taste of adrenaline in my mouth and the overwhelming feeling of powerlessness—all I could do was run. Most of the economically successful white people I have worked with abhor the idea of racism and other forms of discrimination, but those issues are purely theoretical to them. Racism happens at a distance, in other people’s communities, far from the boardroom. Ironically, it’s easier to convince yourself that discrimination isn’t present when--as a direct result of discrimination—there are no people from underrepresented groups present. I see the structural forces that exclude people from influential positions in business as exactly the same as the forces that I saw at work in the streets of New York when I was young. Both apply different sets of rules for different people. Working in the white male-dominated tech startup world, I’ve encountered sexist bias: an unwelcome hand on my knee, being mistaken for a customer service rep, being asked to get coffee, and, of course, being paid less. While I would never compare what I’ve experienced with what it’s like to be Black or brown in America, these things live on a spectrum, all rooted in the same problematic patterns of unequal access to power. Happily, we know that diverse teams are more effective than homogeneous teams. Installing leaders with different backgrounds serves shareholders, employees, and the broader society—even if getting there is easier said than done. For example, the last company I joined had a homogeneous white, engineering team. The reasons for that were complex, but there were some obvious issues. One was that the standard hiring screen included: “Would you like to have a beer with this person?” That question doesn’t sound like it’s “about race,” but most people would rather have a beer with someone just like them; these biases are so natural that most of us don’t even realize that we're discriminating. They’re the foundation of a system that has different rules for different people while pretending to be meritocratic. Thankfully, we know the solution: research shows that hiring executives who are on the flip side of these experiences brings the issues to light and leads to cultures that do, in fact, value peak, holistic performance. And that is why what we’re doing at AboveBoard matters so much. We have the opportunity to create impact at multiple levels: we help executives of all backgrounds get the jobs they want and deserve, we enable companies to hire the very best talent wherever it is, that talent drives the companies’ performance—and all of that together changes the world. With the right solution at the right time and True on our side as a co-founder, we’ve come out of the blocks strong. Even before launch, we had five clients sharing their opportunities with our members: Warburg Pincus, Summit Partners, Audax Group, Insight Partners, and WW (one step from Oprah!) in addition to True. In our first 10 days live, over 1,000 execs joined, 51% of whom are female or an underrepresented minority, and over half of whom are in the C-suite. If you’re an executive reading this, especially a woman, Black, or Latinx executive, I hope you’ll join to be connected with opportunities from companies like Pinterest, GitHub, Ford, Walmart, and Twitch. More than ever before, I am bringing my best full self to this company. It is special for me, weaving the threads of my life into a powerful rope. We are living through immense change, and I’m old enough to know that change comes fastest when it comes from the top. When we transform the face of leadership to reflect the face of America, and beyond, we will be transforming companies from the inside and creating a ripple effect that has the potential to change society. My mission is to drive AboveBoard’s success and create the change that I need to see in the world.  At the end of each How I Built This podcast, the host Guy Raz asks his guests whether their success is based on hard work and skill or luck. I don’t understand how anyone can believe that their achievements were anything but primarily lucky. I have been overwhelmingly lucky:

I believe that the world would be a better place if "successful" people appreciated how important luck was in their journey. Since those people have outsized power, more gratitude should breed more empathy which should result in policies that would be better for those who are less lucky.

I think that people fail to think about compensation broadly enough. This tweet is typical:

Compensation isn't salary. It isn't even salary + incentive comp + equity + benefits. Compensation is all of those things + growth. In a startup, you are usually at a cash disadvantage in recruiting but you have the power of equity and, just as important, the power of growth.

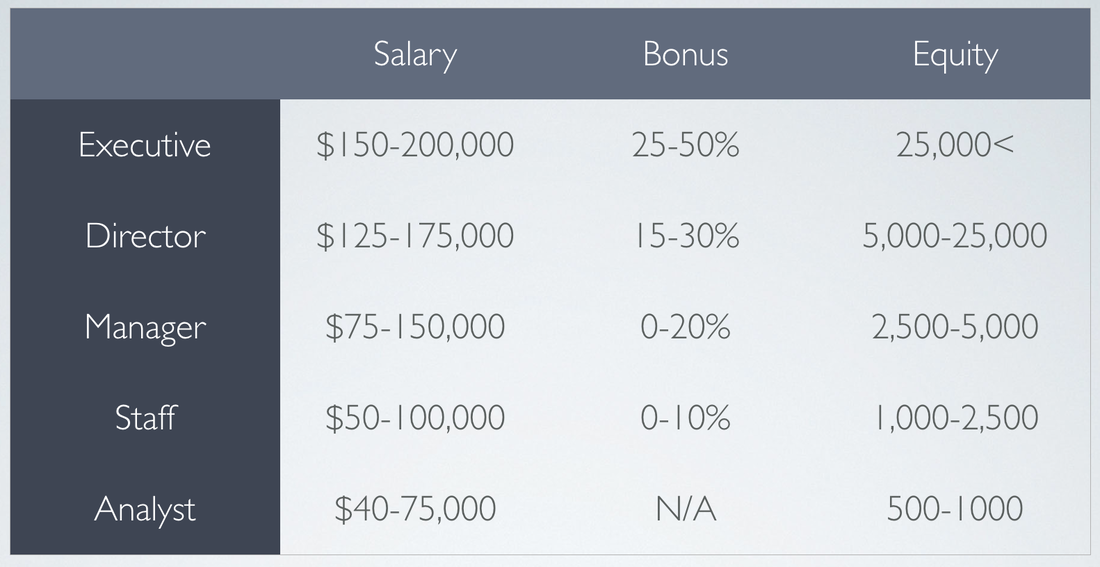

I often hear from founders and CEOs of earlier stage companies that they can't bring on a senior hire they need because they don't have the cash. In that case, you can be outrageously generous with equity. I'm consistently surprised by an unwillingness of an entrepreneur who is stuck in neutral to share significant equity with someone who has the potential to get them moving. The equity will vest, so there is very little downside in giving someone 10, 20, or even 50% of your company in that case. Beyond senior hires, the magic is growth. Trying to convince a young marketer to join my company Real Food Works, I said "I can't guarantee you job security, but I can offer you career security." It sealed the deal and it was true–he's a VP of Marketing now. Out of college I started as a secretary to a VP of Sales for a SF-based startup then called Dial Info, later Automated Call Processing, and ultimately MCI. In four years I went from being a secretary to running a market, to running East Coast operations, and then to becoming a product manager. The opportunity for that kind of trajectory has value–it's compensation. Finally, a personal commitment to help someone grow has value. Being a good coach as well as manager will attract people because it has value to them. It's compensation. The flip side of this approach to selling value as an employer is how to assess a job as a candidate. Look at the numbers, then add the opportunity for growth. And a related note on internships. Until just a few years ago I was a dogged supporter of unpaid work, because I weighed the value of growth so heavily. And then I was enlightened by the argument that unpaid work is discriminatory, because disadvantaged people can't do unpaid work. Duh! I worked from age 15 and certainly couldn't have worked without pay. So, pay people a living wage and give them decent benefits–then add all the growth they can handle. One of the best things about startups is zero bureaucracy. That said, there are a few lightweight structures that add massive value when implemented early. At the top of that list are setting a company cadence–which I'll write about in another post soon–and establishing compensation levels and bands. Banding is the practice of setting standard ranges for salaries, bonuses, and equity by level. As you grow, the matrix will become more complex, but at the beginning, you can start with a simple grid with 4 or 5 levels. Here's an example, with illustrative numbers.  To build you own, get the best market numbers you can (investors often have this data, or Culpepper has a startup offering that's about $2,000.)

Taking the time to set bands lets you make faster compensation decisions: you simply select the relevant band, assess where the candidate should fall within the band, and make the offer. You can get Board approval to make offers within bands simplifying administration. Critically, banding will help you avoid creating compensation disparities that you'll have to rationalize later (which is painful.) I even use the bands to help employees understand where they fit and how they move up. An evening spent creating this simple compensation framework will pay back 10x. |

Categories

All

Archives

May 2021

Me

I blog in spurts, about all sorts of things.

|